Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(34 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(7 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

CBHS International Health

CBHS International Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance

Hunter Health Insurance

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u by HBF

see-u by HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

GU Health

HBF

HCi

HIF

Hunter Health Insurance

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

see-u by HBF

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

More people paying Medicare Levy Surcharge, new ATO data shows

Four-tier system driving up the cost of Gold cover, actuary says

Mind the Gap – private health out-of-pocket costs hit new highs

Family health cover just got more expensive – here’s how to save money

Senior Australians face health insurance double whammy

Bill shock as massive premium increases hit

Gaps for hospital treatment up 7.7%, new data shows

Health insurance premiums rise to 9-year high

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

If you’re having a baby, or thinking about starting a family in the next couple of years, one of the bigger decisions to weigh up is whether it’s worth having health insurance so you can deliver your baby in private care. There’s lots of confusion about what health cover for pregnancy includes and what it excludes, so to help you decide whether to get private health insurance or not, let’s break it down.

What is included in heath cover for pregnancy?

Hospital Cover that includes the Pregnancy and Birth clinical category covers the costs of childbirth in a private hospital, or as a private patient in a public hospital. Despite being named Pregnancy and Birth, it doesn’t actually cover your costs during pregnancy – only during childbirth.

If you have Hospital Cover, here’s what private health insurance for childbirth covers:

- The costs of your labour and delivery, including medications and epidurals

- Specialists’ fees for childbirth, i.e. the obstetrician and anaesthetist

- Midwife fees for childbirth (depending on your policy)

- Hospital accommodation, including your own room (if available)

- Postnatal care while in hospital

- Theatre costs (if you have a caesarean, for example).

If you have Extras Cover, this might help to reduce some of your costs during pregnancy, depending on your policy. Pregnancy treatments covered by Extras Cover include:

What’s covered on Extras Cover?

What isn’t included in health cover for pregnancy?

Many people who opt for a private hospital delivery do so because they like being able to choose their own obstetrician, but might not realise that appointments in the obstetrician’s clinic (or with your GP) before and after the birth won’t be covered by health insurance. That’s because Hospital Cover only includes treatments inside of hospital.

Here’s what else isn’t included:

- Pregnancy tests and scans, e.g. blood tests and ultrasounds. Some of these costs will be covered by Medicare, but there may be a Gap for you to pay.

- Costs to treat your baby if they’re admitted to hospital, e.g. following a premature or multiple birth. You’ll need to upgrade to a Single parent or Family policy ahead of the birth for your baby to be covered.

- Post-birth check-ups for your baby outside hospital, e.g. with a paediatrician or GP.

What are the Gaps for obstetrician fees?

Medical Costs Finder says the average Gap paid for a vaginal delivery without complications was $420, while a caesarean without complications resulted in an average Gap of $500. But it’s important to know that obstetrician fees can be high, meaning out-of-pocket costs may be much higher than that average. According to the ABC, obstetrician costs in Sydney could be as high as $8,000, so make sure you get a full breakdown of costs from your doctor ahead of time and check with your insurer about what’s covered.

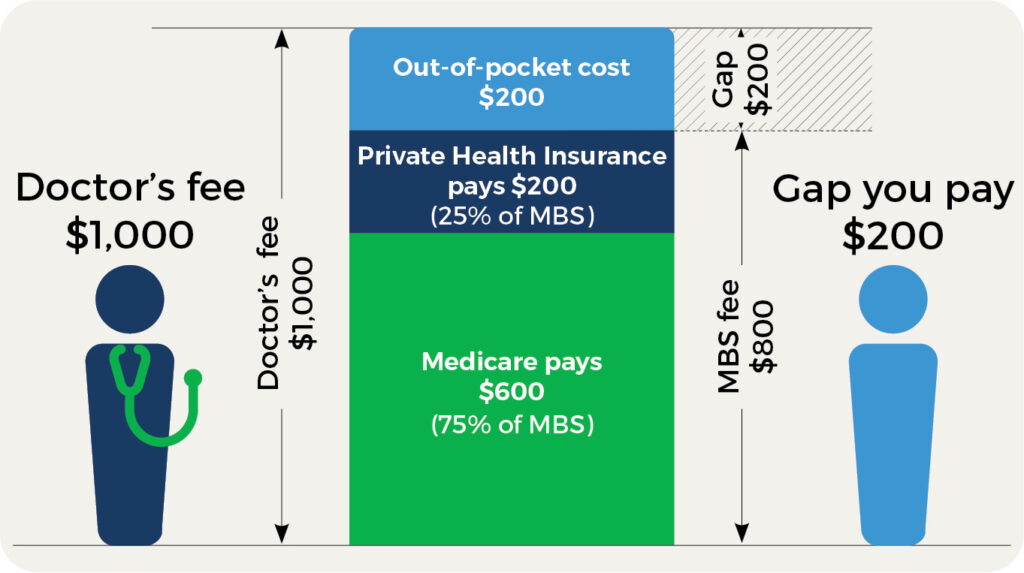

If you have Hospital Cover, why is there a Gap? When you’re admitted for labour and delivery, Medicare will cover 75% of the Medicare Benefits Schedule (MBS) Fee, and your health insurance will cover the remaining 25%. But if your obstetrician charges more than the MBS (and many do), that leaves a Gap for you to pay.

Here’s an example of how doctor’s fees higher than the MBS can create a Gap:

What’s the best health cover for pregnancy?

Pregnancy and Birth is usually only covered on the Gold tier (the most expensive level) of Hospital Cover, but we found a handful of Silver Plus policies that included Pregnancy and Birth, so it pays to shop around. Surprisingly, the cheapest policy for one adult in Queensland that covered Pregnancy and Birth – which we found using the healthslips.com.au calculator – was actually a Gold policy costing $236.05 a month, with a $750 excess. By contrast, the most expensive was a Gold policy for $480.18 a month, with a $750 excess.

What are the different tiers of Hospital Cover?

Don’t forget – if you want your baby to be covered for care they might need if they’re unwell, you’ll need to upgrade to a Single parent or Family policy before the birth.

healthslips.com.au does not provide general or personalised advice. Your particular circumstances are likely to impact the accuracy, completeness and relevance of the information or results. Take this into account before making a decision and talk to an expert for financial advice.

Trudie McConnochie

Writer and Researcher

Knowledge is power – that’s the guiding principle behind everything Trudie writes, and it’s a philosophy she brings to her work at healthslips.com.au. By breaking down complex information into easy-to-understand blogs and stories, she aims to empower Australians to make the best choices and an informed decision around private health insurance.

Trudie understands firsthand some of the complexity of private health insurance having moved to Australia from New Zealand and having to navigate a vastly different public healthcare system and health insurance structure.

Trudie holds a Bachelor of Communication Studies (journalism major) from the Auckland University of Technology.

Policies change monthly, stay informed

Subscribe to stay informed. Insurers regularly update policies, introduce new policies and close policies. Our data is updated monthly.