Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(34 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(7 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

CBHS International Health

CBHS International Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance

Hunter Health Insurance

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u by HBF

see-u by HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

GU Health

HBF

HCi

HIF

Hunter Health Insurance

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

see-u by HBF

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

Mind the Gap – private health out-of-pocket costs hit new highs

Family health cover just got more expensive – here’s how to save money

Senior Australians face health insurance double whammy

Bill shock as massive premium increases hit

Gaps for hospital treatment up 7.7%, new data shows

Health insurance premiums rise to 9-year high

Higher Gaps forcing many people to delay care, survey finds

Health insurance giving Aussies less value, doctors say

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

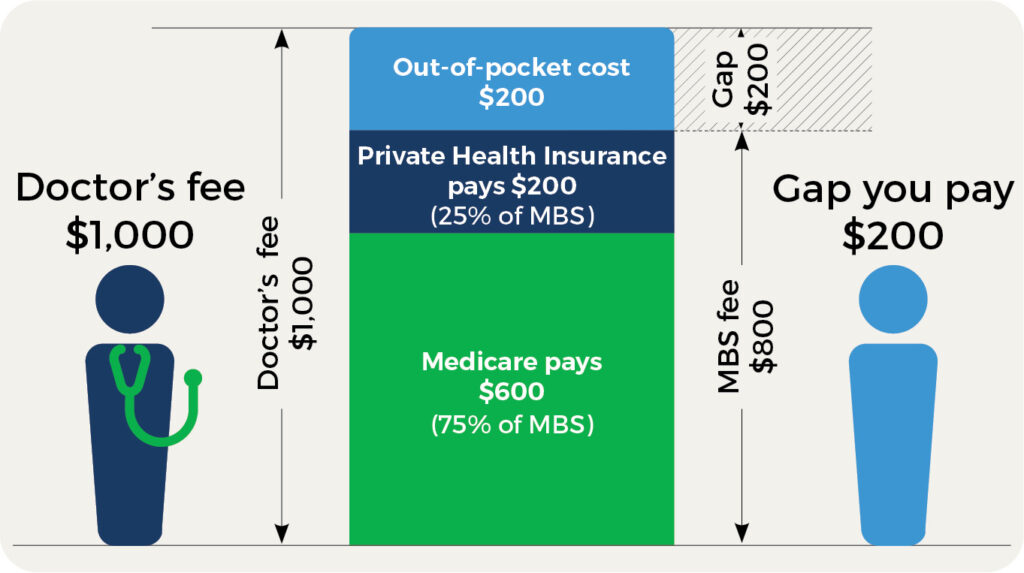

If you’re using Hospital Cover to pay for surgery or a hospital procedure as a private patient, you probably assume your insurer will pick up the bill. But unfortunately health insurance doesn’t always cover 100% of the private hospital costs – sometimes there will be out-of-pocket costs, also known as Gaps.

So what is a Gap? A Gap is the out-of-pocket cost you are responsible for paying. The price of a hospital procedure is known as the Medicare Benefit Schedule Fee (MBS Fee), and it will be covered by Medicare and your private health insurer combined. However sometimes specialist fees are higher than the MBS Fee, which leaves a Gap for you to pay – this is known as a Medical Gap.

There are 2 types of Gaps you might face for a Hospital Cover claim, which apply whether you’re in a private hospital or you’re a private patient in a public hospital:

- Medical Gap – for doctor and specialist fees. When specialist fees are higher than the MBS Fee, you will have a Medical Gap to pay

- Hospital Gap – for hospital fees, including theatre costs and accommodation. When a private hospital charges more than what your health insurer will pay, the difference is a Hospital Gap that you will have to pay.

If you’re facing a hospital procedure as a private patient and want to reduce your out-of-pocket costs, here are our top 4 tips.

How to lower out-of-pocket costs for private hospital treatment

1. Get a cost breakdown

When your doctor or specialist recommends you for hospital treatment, ask for a full breakdown of fees. Make sure it includes the MBS item number and fees for all doctors involved including anaesthetists, and hospital costs such as accommodation. Then, compare that against average fees and Gaps for that procedure, using the government’s Medical Cost Finder website. This will tell you whether the Gap is in the normal range.

2. Look for a different provider

If you have to pay a Medical Gap, the first step is to look for a different provider who charges a lower (or no) Gap. Phone other specialists’ practices and quote your MBS item number – they can tell you how much the specialist charges for that service. It’s also a good idea to contact your insurer and ask whether they have ‘no Gap’ or ‘known Gap’ arrangements with relevant specialists. Some insurers provide an online search option for healthcare providers, like this one from HCF.

Tip:

Even if specialists have an agreement with your insurer, they aren’t obligated to honour it. Ask your specialist to confirm in writing whether they will honour their ‘no Gap’ or ‘known Gap’ agreement with your insurer.

3. Change hospitals

If you’re being treated in a private hospital you could face a Hospital Gap for costs such as accommodation and theatre fees.

Many insurers have arrangements with certain hospitals, known as Agreement Hospitals. This means members can get treatments with either no Hospital Gap or a ‘known’ Hospital Gap (at a capped amount). If your specialist has recommended treatment at a hospital which doesn’t have an agreement with your insurer, ask them whether your procedure can be done in one of your insurer’s Agreement Hospitals. You can ask your insurer for a list of their Agreement Hospitals, or search here.

By the way, there usually isn’t a Hospital Gap if you’re being treated as a private patient in a public hospital.

4. Change policies

If you’re disappointed by the cover on your policy, changing policies could help you lower out-of-pocket costs – but only if you change to a policy at the same level with the same excess (if you change to a higher tier you’ll have to serve a waiting period before you can claim). Finding health insurance might sound time-consuming, but at healthslips.com.au we’ve taken the hard work out, creating a handy Calculator that lets you search every policy from every insurer in Australia in a matter of seconds. We give you all your policy options with no bias, and you don’t have to sign up or give any contact details to get your results. It’s fast and it’s free – try looking for a new policy or compare your current policy with others today.

Trudie McConnochie

Writer and Researcher

Knowledge is power – that’s the guiding principle behind everything Trudie writes, and it’s a philosophy she brings to her work at healthslips.com.au. By breaking down complex information into easy-to-understand blogs and stories, she aims to empower Australians to make the best choices and an informed decision around private health insurance.

Trudie understands firsthand some of the complexity of private health insurance having moved to Australia from New Zealand and having to navigate a vastly different public healthcare system and health insurance structure.

Trudie holds a Bachelor of Communication Studies (journalism major) from the Auckland University of Technology.

Policies change monthly, stay informed

Subscribe to stay informed. Insurers regularly update policies, introduce new policies and close policies. Our data is updated monthly.