Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(34 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(7 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

CBHS International Health

CBHS International Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance

Hunter Health Insurance

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u by HBF

see-u by HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

GU Health

HBF

HCi

HIF

Hunter Health Insurance

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

see-u by HBF

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

More people paying Medicare Levy Surcharge, new ATO data shows

Four-tier system driving up the cost of Gold cover, actuary says

Mind the Gap – private health out-of-pocket costs hit new highs

Family health cover just got more expensive – here’s how to save money

Senior Australians face health insurance double whammy

Bill shock as massive premium increases hit

Gaps for hospital treatment up 7.7%, new data shows

Health insurance premiums rise to 9-year high

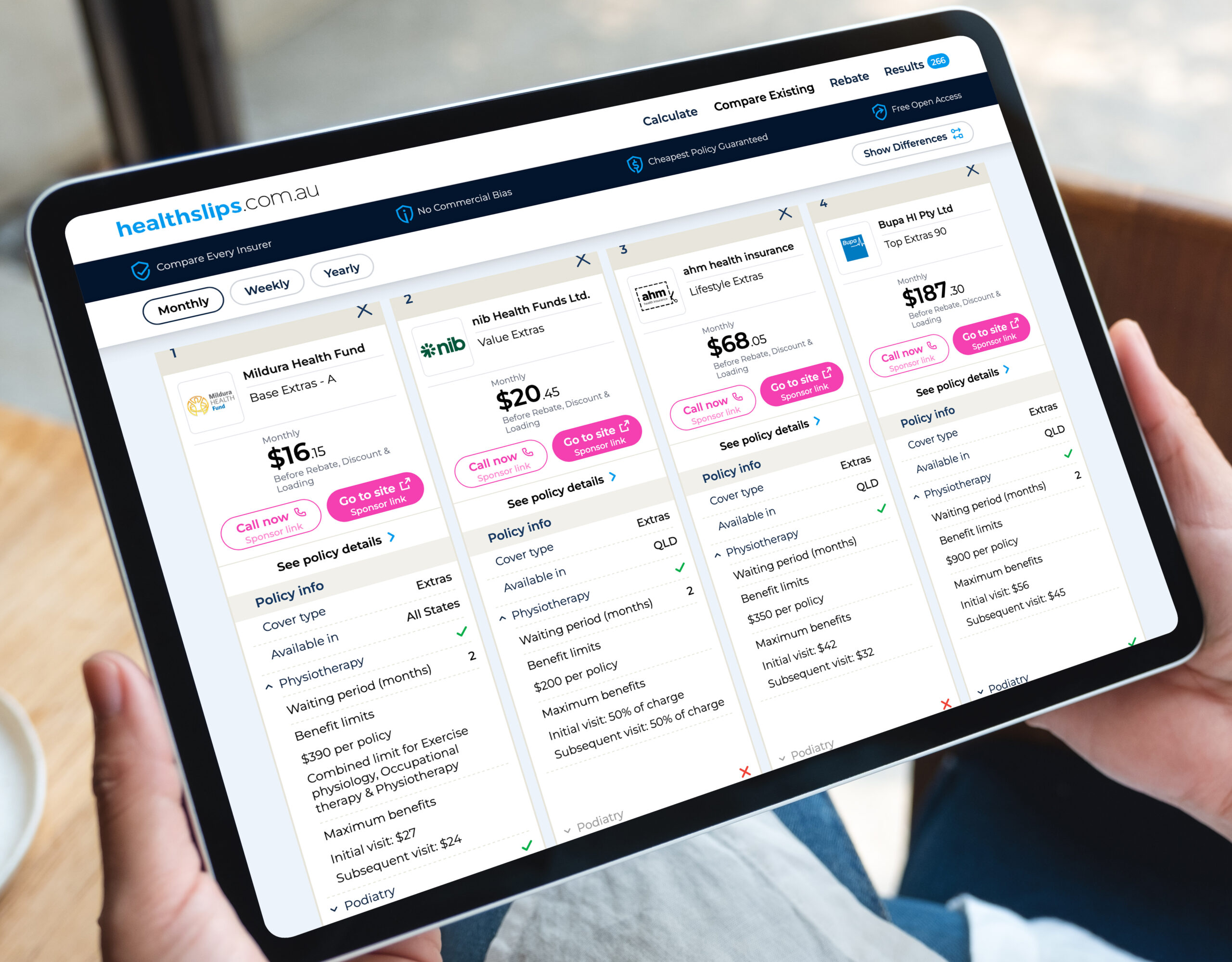

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

If you’re in your 20s, you might find yourself considering health insurance for the first time. Maybe you:

- need health cover to reduce your tax

- are facing some hospital treatments

- were covered by your parents’ policy and now need your own.

Whatever your situation, at healthslips.com.au we’re here to make health insurance easy to understand – what you need, how much it costs – without the jargon or sales pressure.

On this page

- Do I need health insurance in my 20s?

- How much does health insurance cost in your 20s?

- What type of health insurance should I get?

- Incentives and penalties to know in your 20s

- How do I choose health insurance in my 20s?

Do I need health insurance in my 20s?

You don’t have to take out private health insurance in your 20s because Medicare covers you for treatment in a public hospital. But many young Australians choose it for flexibility, faster treatment and financial reasons.

Why people in their 20s get health insurance?

People in their 20s usually get health insurance for one (or more) of these reasons:

- Avoid paying extra tax with the Medicare Levy Surcharge.

- Skip long public hospital wait times and plan ahead for surgery, chronic conditions or pregnancy.

- Save money on dental, physio, optical and mental health services such as psychology.

- Lock in discounts and avoid higher premiums later by joining before age 31.

- Having to leave their parents policy. (Note: some insurers allow you to remain on your parents’ policy until age 31. Check your parents’ policy for details.)

Chloe, leaving her parents’ policy

Chloe is 22 and was covered by her parents’ health insurance previously. She does not want Hospital Cover because she earns $65,000 and can avoid the Medicare Levy Surcharge. She decides to get Extras Cover to cover some of her dental treatment costs.

How much does health insurance cost in your 20s?

Health insurance prices vary based on policy type (Hospital or Extras) and what’s covered – not your age.

There are 4 tiers of Hospital Cover to consider: Basic, Bronze, Silver and Gold. The difference between each tier lies in the number of treatments covered.

Basic, Bronze and Silver tiers offer ‘Plus’ policies with additional services. A Basic Hospital Cover policy offers minimal cover, whereas a Basic Plus policy covers more hospital services and treatments for a little more money. If you’re considering starting a family and want to be covered for private childbirth, you’ll need to choose a policy that covers Pregnancy and Birth – which is available on a few Silver Plus policies and all Gold policies. There will be a 12-month waiting period before you can claim for childbirth, so you’ll need to take out cover before getting pregnant (find out more in our Starting a Family guide).

For a single adult, no kids, living in NSW, here are some price comparisons, as at April 2026:

Cheapest Hospital Cover

- Basic – $102.60/month, $750 excess, ahm health insurance ambulance hospital (basic)

- Bronze – $121.79/month, $750 excess, see-u by HBF Saver Hospital $750 Excess with Daily Co-Pay (Bronze Plus)

- Silver – $157.30/month, $750 excess, ahm health insurance essentials silver plus

- Gold – $248.55/month, $750 excess, Mildura Health Fund Five Star Gold $750 Excess – F4

Being under 30 can make you eligible for discounts that reduce your premium.

Basic, Basic Plus or Bronze Hospital Cover is usually the cheapest way to avoid the Medicare Levy Surcharge.

How much does Extras Cover cost?

Extras Cover costs less than Hospital Cover, but doesn’t reduce your tax. For a single person in their 20s, no kids, living in NSW, here are some Extras Cover price comparisons, as at April 2026:

- Cheapest Extras Cover – $22.16/month, HBF Health Smart Start Extras, which covers 9 of 27 treatments including General Dental, Optical and Physio.

- Most Expensive Extras Cover – $217.10, Bupa Health Insurance Top Extras 90, which covers 25 of 27 treatments.

How much does Combined cover cost?

Combined cover includes both Hospital and Extras Cover. For a single person in their 20s, no kids, living in NSW, here are some price comparisons based on Silver tier Hospital Cover, as at April 2026:

- Cheapest Combined Cover – $178.45/month, $750 excess, see-u by HBF Secure Hospital $750 Excess (Silver) & Starter Extras, which covers 29 of 38 Hospital Cover clinical categories and 8 of 27 Extras treatments including General Dental, Optical and Physio.

- Most Expensive Combined Cover – $529.40, $750 excess, AIA Health Insurance Silver Plus Family Hospital 750 and Best 70% Back Extras, which covers 37 of 38 Hospital Cover clinical categories and 25 of 27 Extras treatments.

Use the healthslips.com.au calculator to compare every policy in Australia ranked cheapest to most expensive – instantly and free.

What type of health insurance should I get?

The right cover depends on what you want it for – saving tax, reducing health costs or peace of mind.

- Hospital Cover – covers the cost of treatment in a private hospital, or as a private patient in a public hospital. Hospital Cover helps you get non-urgent surgery faster, choose your own doctor and get your own room (if available). Hospital Cover helps you avoid paying the Medicare Levy Surcharge if your income is over the MLS threshold.

What health treatments are covered by Hospital Cover?

- Extras Cover – helps cover the cost of a range of treatments that Medicare does not cover, such as dental, physio, optical and psychology. Extras Cover doesn’t cover all of your treatment cost and there’s an annual limit. Keep in mind: Extras Cover does not affect the Medicare Levy Surcharge.

What health treatments are covered by Extras Cover?

- Combined Cover – includes Hospital Cover and Extras Cover.

- Ambulance Cover – Medicare doesn’t cover ambulance treatment, but if you have Ambulance Cover your ambulance treatment costs are covered. Ambulance treatment is often included with Hospital Cover and Extras Cover policies, so you may not need Ambulance Only Cover if you have other health insurance. (Note: not required for QLD or TAS residents because your state governments fund ambulance costs.)

Who should I include on my policy?

- Single – covers one adult.

- Couple – covers 2 adults in a relationship, living together (you don’t have to be married)

- Single Parent – covers one adult and one or more children.

- Family – covers 2 adults in a relationship, living together, with one or more children.

Compare all cover types and the cost of including a partner and children in your policy using the healthslips.com.au calculator. It’s fast, easy and free.

Jade & Kim, different health needs

Jade, 27, and Kim, 28, are a couple who have lived together for a year. They want to get Hospital Cover so they can avoid paying the Medicare Levy Surcharge. Jade has type 1 diabetes and wants cover for insulin pumps, but Kim doesn’t need a high level of cover, so they decide to get 2 Singles policies. Jade buys a Gold tier policy to cover her insulin pumps, while Kim buys a Basic Plus policy to give her a basic level of cover.

If you’re under the age of 31 and single, you may be eligible for cover on your parents’ policy. Check your parents’ health insurance policy for details.

Incentives and penalties to know in your 20s

Government incentives can significantly affect how much you pay, especially if you buy Hospital Cover before turning 31.

- Government Rebate – reduces your health insurance premium based on your income and number of children. Check your eligibility.

- Age-based Discount – reduces your Hospital Cover premium if you start cover before 30, and if you maintain your policy, you may keep the Discount until the age of 41. Not available from all insurers. Check details here.

- Lifetime Health Cover Loading – increases your Hospital Cover premium if you don’t take out cover before the age of 31. It’s a good reason to consider taking out a policy in your 20s. Get all the details here.

Also remember the Medicare Levy Surcharge (MLS), which isn’t a penalty – it’s a type of tax if you earn more than $105,000 (as a single person). It applies to anyone earning over a certain income level who doesn’t have Hospital Cover.

Do I have to pay the Medicare Levy Surcharge?

Tim, wants to avoid the MLS and Loading

Tim is 28 and earns $110,000. He decides to get Hospital Cover so he can avoid the Medicare Levy Surcharge, and avoid the Lifetime Health Cover Loading by buying cover before he turns 31. He is planning to move to the UK next year for 2 years so will cancel his policy and buy a new policy when he returns to Australia.

Liam, plays competitive footy

Liam is 28, plays competitive footy regularly. He knows he’s at higher risk of injury but decides he’s happy to be treated in the public hospital system. His income is $80,000 so he doesn’t have to pay the Medicare Levy Surcharge. He decides to wait until his 30s to get health insurance.

How do I choose health insurance in my 20s?

Here are the 4 easy steps to choosing a health insurance policy in your 20s:

- Choose your type of cover

If you want to avoid the Medicare Levy Surcharge, you’ll need Hospital Cover. If you want cover for out-of-hospital treatments like dental and physio, you’ll need Extras Cover. Choose Hospital Cover, Extras Cover or both, based on your health needs and budget. - Choose what treatments you need covered

If you have a health condition, or a family predisposition to a particular illness, look for a policy that meets those needs. - Search for the cheapest policy that meets your needs and budget

The healthslips.com.au calculator searches every policy from every insurer without any commercial bias. See your results instantly without entering your name, email or phone number. - Buy your policy

Once you’ve found the right policy, double-check the details – including waiting periods and excess. You’ll be covered as soon as you’ve paid your first premium, but there may be waiting periods before you can claim.

Angie, planning for surgery

Angie is 24 and has been diagnosed with endometriosis. Her doctor has told her she may need surgery in the future and there could be a long wait in the public system. She buys a Bronze Hospital Cover policy that includes the Gynaecology clinical category. Although there is a 12-month waiting period for pre-existing conditions, she is happy to wait as she will likely not need surgery in the next year.

Helpful articles

Leaving your parents’ health insurance and getting your own policy? What you need to know

Is health insurance worth having?

Does health insurance cost less if I’m healthy?

Can I get private health insurance with pre-existing conditions?

What’s the cheapest health insurance to avoid the Medicare Levy Surcharge?

Policies change monthly, stay informed

Subscribe to stay informed. Insurers regularly update policies, introduce new policies and close policies. Our data is updated monthly.