Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(34 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(7 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

CBHS International Health

CBHS International Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance

Hunter Health Insurance

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u by HBF

see-u by HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

GU Health

HBF

HCi

HIF

Hunter Health Insurance

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

see-u by HBF

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

More people paying Medicare Levy Surcharge, new ATO data shows

Four-tier system driving up the cost of Gold cover, actuary says

Mind the Gap – private health out-of-pocket costs hit new highs

Family health cover just got more expensive – here’s how to save money

Senior Australians face health insurance double whammy

Bill shock as massive premium increases hit

Gaps for hospital treatment up 7.7%, new data shows

Health insurance premiums rise to 9-year high

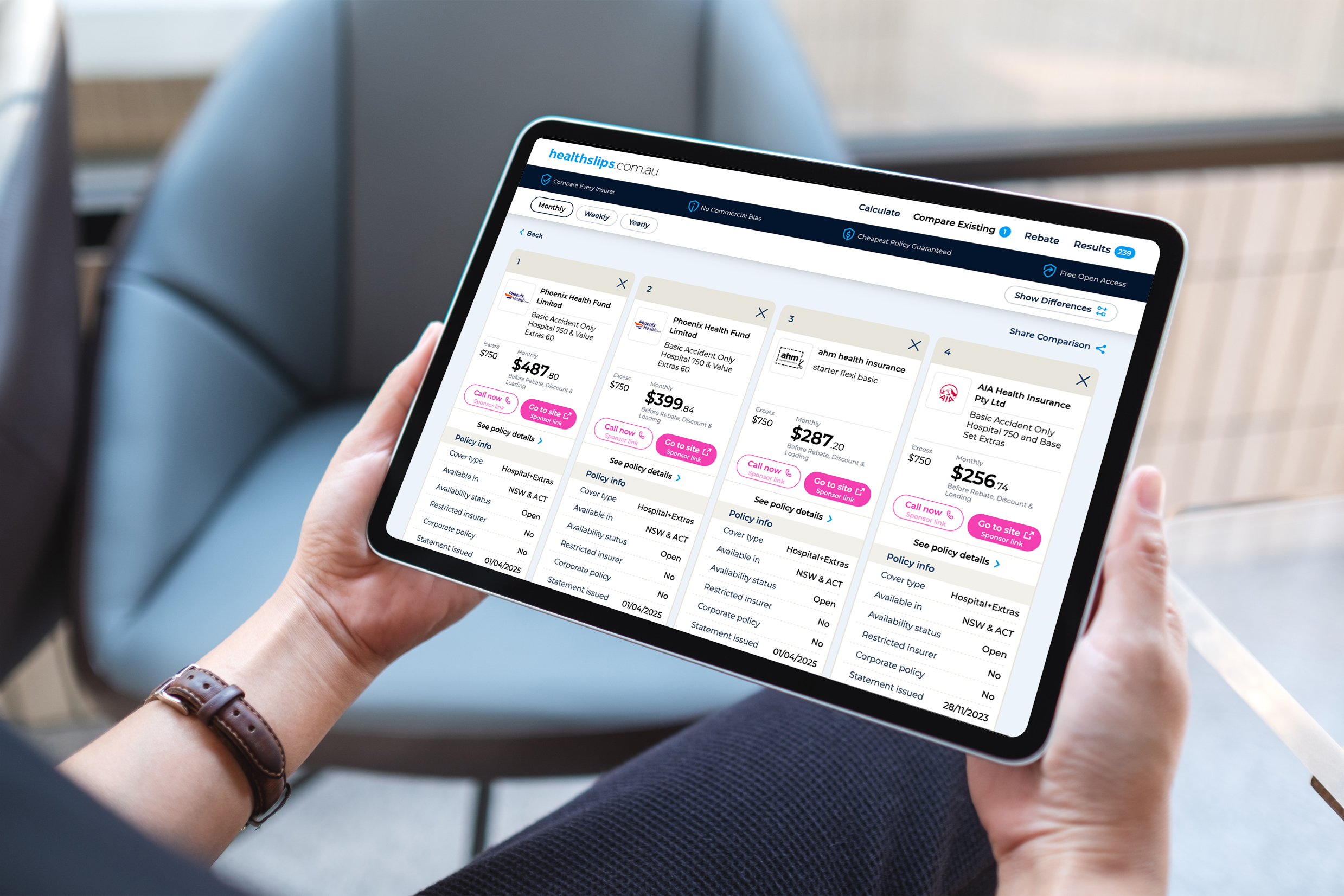

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

Whether you’re enjoying good health or facing hospital treatment, there are many reasons to consider health insurance in your senior years:

- access private hospital treatment for surgery

- reduce the costs of non-hospital health appointments

- avoid extra tax.

Whatever your motivation for considering health insurance in the second half of your life, we’re here to help you understand policy options, costs and government penalties.

On this page:

Do I need health insurance in my senior years?

Public hospital care is free under Medicare, so having private health insurance isn’t essential. But in your senior years, your likelihood of hospitalisation goes up, so many people choose Hospital Cover for faster access to non-urgent surgery.

People get health insurance in their senior years for a range of reasons including:

- Skip long public hospital wait times with faster access to treatment in a private hospital, especially for common procedures like cataracts and joint replacements

- Choose your own doctor and potentially your own room (if available) in a private hospital

- Avoid paying the Medicare Levy Surcharge (MLS), if your income from salary, investments, pension and superannuation exceeds the threshold

- Reduce out-of-pocket costs for dental, physio, audiology and osteo.

Delia, wants to avoid wait times

Delia, 61, is considering getting a policy so she can get treated in a private hospital faster if she needs to in the future. Her sister waited several months for cataract surgery and Delia wants to make sure she doesn’t have to wait that long if she develops health problems. She buys a Gold tier Hospital Cover that covers everything including ambulance treatment, but decides Extras Cover doesn’t make sense for her health needs. Because she hasn’t had Hospital Cover before, she must pay an extra 62% Lifetime Health Cover on top of her premium.

Find out how to choose health insurance for elderly parents.

How much does health insurance cost for seniors?

The cost of health insurance depend on what treatments and services are covered, not your age.

There are 4 Hospital Cover tiers: Basic, Bronze, Silver and Gold, as well as ‘Plus’ policies (in Basic, Bronze and Silver) which provide more cover at each level.

For a couple in their 70s living in Victoria, here are some price comparisons as at April 2026:

Cheapest Hospital Cover

- Basic – $204.20/month, $750 excess, ahm health insurance ambulance hospital (basic)

- Bronze – $255.86/month, $750 excess, see-u by HBF Saver Hospital $750 Excess with Daily Co-Pay (Bronze Plus)

- Silver – $338.10/month, $750 excess, HBF Health Essential Silver Hospital $750/$1500 Excess

- Gold – $497.10/month, $750 excess, Mildura Health Fund Five Star Gold $750 Excess – F4

Your medical history and age won’t affect your premiums. However if you haven’t maintained Hospital Cover since your 20s, you’ll pay a government penalty called the Lifetime Health Cover Loading which will increase your premium.

How much does Extras Cover cost?

Extras Cover is for non-hospital healthcare services not covered by Medicare, including dental, physio and optical. For a couple in their 70s living in Victoria, as at April 2026:

- Cheapest Extras Cover – $43.28/month, HBF Health Smart Start Extras, which covers 9 treatments including General Dental, Optical and Physio.

- Most Expensive Extras Cover – $408.20/month, Bupa Health Insurance Top Extras 90, which covers 25 of 27 treatments.

How much does Combined Cover cost?

Combined Cover is Hospital and Extras cover in one package. It doesn’t make cover cheaper than buying each policy separately, but it means only one payment. For a couple in their 70s living in Victoria, here are some price comparisons for Silver tier cover, as at April 2026:

- Cheapest Combined Cover – $376.60/month, $750 excess, Frank Health Insurance Silver Hospital & Bundables $250, which covers 29 of 38 Hospital Cover clinical categories and 13 of 27 Extras Cover treatments, including General Dental, Optical and Physio.

- Most Expensive Combined Cover – $1,012.04/month, $750 excess, AIA Health Insurance Silver Plus Family Hospital 750 and Best 70% Back Extras, which covers 37 of 38 Hospital Cover clinical categories and 25 of 27 Extras Cover treatments.

What type of health insurance should I get?

You can buy health insurance for just yourself (a Single policy), or if you’re living with a partner, you might choose a Couples policy. The type of cover depends on what health treatments you want covered.

- Hospital Cover – covers treatment as a private patient so you can get elective surgery faster and choose your own doctor. What health treatments are covered by Hospital Cover? It also helps you avoid the Medicare Levy Surcharge if your combined income is over the threshold.

- Extras Cover – helps cover the cost of a range of treatments that Medicare does not cover, such as dental, physio, optical and psychology. It doesn’t cover 100% of appointment costs and there are annual limits. What health treatments are covered by Extras Cover? Remember that Extras Cover won’t help you avoid the Medicare Levy Surcharge.

- Combined Cover – includes Hospital Cover and Extras Cover. It won’t necessarily save you money to buy 2 policies this way.

- Ambulance Cover – Medicare doesn’t cover ambulance treatment, so Ambulance Cover can help you avoid the cost for ambulance treatment. You may not need Ambulance Only Cover if you have other health insurance as it’s often included. (Note: if you live in Queensland or Tasmania, ambulance costs are paid for by your state government.)

Compare all cover types and the cost of including a partner and children in your policy using the healthslips.com.au calculator. It’s fast, easy and free.

Robert, wants knee replacement cover

Robert, 76, has been living with knee osteoarthritis for years and has been told he may need a knee replacement later down the track. He knows public hospital wait lists are long, so he checks his Bronze tier Hospital Cover policy, but finds that knee replacements are not covered. He uses the healthslips.com.au calculator and finds a Silver Plus tier policy that covers joint replacements. He upgrades to the new policy, and although he will have a 12-month waiting list before he can claim for knee replacements, the doctor tells him he is unlikely to need surgery in that period.

Incentives and penalties to know in your senior years

How much you pay for health insurance is affected by government incentives and penalties:

- Private Health Insurance Rebate – reduces premiums if you earn below the income thresholds. If you’re aged over 65, your rebate could be more.

- Lifetime Health Cover Loading – adds 2% to Hospital Cover premiums for every year you’re over 30 when you first take out cover, up to a maximum of 70%. This is removed after 10 years of continuous cover.

Don’t forget about the Medicare Levy Surcharge (MLS). It doesn’t affect premiums but does mean an extra 1-1.15% tax if you earn over the threshold and don’t have Hospital Cover for the full financial year.

Maria and Benjamin, considering Hospital Cover

Maria and Benjamin are a couple in their 70s. They had health insurance when their children were young but cancelled their policy many years ago to save money. They are worried about their health needs in the future so they are considering getting a new policy. Because they cancelled their previous policy, they will need to pay Lifetime Health Cover Loading – which will add 70% to their Couples policy. Because of this cost they decide not to get cover and rely on the public health system instead.

How do I choose health insurance in my senior years?

Here are 4 simple steps:

- Choose your cover type

Choose Hospital Cover, Extras Cover or both, based on your health needs and budget. If you want access to private hospital treatment, you’ll need Hospital Cover. If you want cover for non-hospital treatments like dental and physio, you’ll need Extras Cover. Check that ambulance cover is included, or buy an Ambulance-Only Cover policy if that’s important to you.

- Choose your treatments

If you have a health condition, or a family predisposition to a particular illness, look for a policy that meets your health needs.

- Compare policies

With the free healthslips.com.au calculator, you can search every policy in Australia without commercial bias, and we guarantee you the cheapest policy.

- Buy your policy

Before you buy, check waiting periods, excess and any incentives or penalties. You’ll be covered once you’ve paid your first premium, but will face waiting periods before you can claim.

Cathy, wants Extras Cover

Cathy, 82, has had Hospital Cover for many years but is considering Extras Cover to help with her costs for audiology, dental, optical, physio and podiatry appointments. She uses the healthslips.com.au calculator and finds a Combined Hospital and Extras Cover policy that involves the same level of Hospital Cover as her existing policy for a lower price, plus a mid-level Extras Cover policy to reduce her non-hospital health appointments. She works out that she would claim enough back each year to make the Extras Cover policy financially viable.

Helpful articles

What’s the best health insurance for Aussie seniors?

How much should I get back from health insurance?

Can I claim dentures on health insurance?

Can I get health insurance with pre-existing health conditions?

How health insurance can support you with arthritis

Does health insurance cover cataract surgery?

Policies change monthly, stay informed

Subscribe to stay informed. Insurers regularly update policies, introduce new policies and close policies. Our data is updated monthly.