Guides Overview

Australian Health System

(25 articles)

Health Insurance Prices

(20 articles)

Private Health Insurance

(34 articles)

Private Health Insurers

(15 articles)

Medicare

(28 articles)

Medicare Benefits Schedule (MBS)

(6 articles)

Pharmaceutical Benefits Scheme (PBS)

(8 articles)

Public Hospitals

(6 articles)

Private Hospitals

(7 articles)

Medicare Levy

(7 articles)

Private Health Insurance Rebate

(7 articles)

Age-based Discount

(5 articles)

Lifetime Health Cover Loading

(11 articles)

Insurers Overview

AAMI Health Insurance

AAMI Health Insurance

ACA Health

ACA Health

ahm

ahm

AIA Health Insurance

AIA Health Insurance

Allianz Care Australia

Allianz Care Australia

APIA Health Insurance

APIA Health Insurance

Astute Simplicity Health

Astute Simplicity Health

Australian Unity

Australian Unity

Bupa Health Insurance

Bupa Health Insurance

CBHS Corporate

CBHS Corporate

CBHS Health

CBHS Health

CBHS International Health

CBHS International Health

Defence Health

Defence Health

Doctors’ Health

Doctors’ Health

Emergency Services Health

Emergency Services Health

Frank

Frank

GMHBA

GMHBA

GU Health

GU Health

HBF

HBF

HCF

HCF

HCi

HCi

Health Partners

Health Partners

HIF

HIF

Hunter Health Insurance

Hunter Health Insurance

ING Health Insurance

ING Health Insurance

Latrobe Health Services

Latrobe Health Services

Medibank

Medibank

Mildura Health Fund

Mildura Health Fund

Navy Health

Navy Health

nib

nib

Nurses & Midwives Health

Nurses & Midwives Health

onemedifund

onemedifund

Peoplecare

Peoplecare

Phoenix Health Fund

Phoenix Health Fund

Police Health

Police Health

Priceline Health Insurance

Priceline Health Insurance

Qantas Insurance

Qantas Insurance

Queensland Country Health Fund

Queensland Country Health Fund

Real Health Insurance

Real Health Insurance

Reserve Bank Health Society (RBHS)

Reserve Bank Health Society (RBHS)

RT Health

RT Health

see-u by HBF

see-u by HBF

Seniors Health Insurance

Seniors Health Insurance

St Lukes Health

St Lukes Health

Suncorp Health Insurance

Suncorp Health Insurance

Teachers Health

Teachers Health

Territory Health Fund

Territory Health Fund

Transport Health

Transport Health

TUH

TUH

UniHealth

UniHealth

Union Health

Union Health

Westfund

Westfund

AAMI Health Insurance

ACA Health

ahm

AIA Health Insurance

Allianz Care Australia

APIA Health Insurance

Astute Simplicity Health

Australian Unity

Bupa Health Insurance

CBHS Corporate

CBHS Health

Defence Health

Emergency Services Health

Frank

GU Health

HBF

HCi

HIF

Hunter Health Insurance

Mildura Health Fund

Navy Health

nib

Nurses & Midwives Health

Police Health

Reserve Bank Health Society (RBHS)

see-u by HBF

St Lukes Health

Teachers Health

Transport Health

TUH

UniHealth

Westfund

News Overview

More people paying Medicare Levy Surcharge, new ATO data shows

Four-tier system driving up the cost of Gold cover, actuary says

Mind the Gap – private health out-of-pocket costs hit new highs

Family health cover just got more expensive – here’s how to save money

Senior Australians face health insurance double whammy

Bill shock as massive premium increases hit

Gaps for hospital treatment up 7.7%, new data shows

Health insurance premiums rise to 9-year high

Calculate Cheapest Policy

Search for a new policy based on your health cover needs and budget. We compare every insurer and every policy.

Whether you’re fit and healthy or you’re facing hospital treatments, there are lots of reasons to consider health insurance in your 30s. Maybe you want to:

- avoid extra tax as your income grows

- plan ahead for surgery or ongoing health needs

- start (or grow) a family

- protect your health as you get older.

Whatever your reason, we’re here to help you understand your options, compare costs and choose health insurance that fits you – without the jargon or sales pressure.

On this page

Do I need health insurance in my 30s?

You can be treated for free in a public hospital under Medicare, but many people in their 30s choose health insurance.

Why people in their 30s get health insurance

People in their 30s may get health insurance for one (or more) of these reasons:

- Avoid paying extra tax with the Medicare Levy Surcharge (MLS)

- Skip long public hospital wait times with faster access to treatment in a private hospital

- Reduce out-of-pocket costs for dental, physio and psychology

- Lock in cover earlier to limit Lifetime Health Cover Loading later

- Access private childbirth options (find out more in our Starting a Family guide).

Priya, planning ahead

Priya is 34 and regularly runs marathons. She already has Extras Cover to reduce her physio and massage costs, but decides to get Hospital Cover as well, in case she experiences any injuries that need surgery. Hospital Cover will allow her to have the procedure done in a private hospital and get back to training faster.

How much does health insurance cost in your 30s?

The cost of health insurance depend on what’s covered, not your age.

There are 4 Hospital Cover tiers: Basic, Bronze, Silver and Gold. Also available are ‘Plus’ policies (in Basic, Bronze and Silver) which cover more treatments.

For a single adult in their 30s, no kids, living in Queensland, here are some price comparisons as at April 2026:

Cheapest Hospital Cover

- Basic – $102.99/month, $750 excess, see-u by HBF Starter Hospital $750 Excess with Daily Co-Pay (Basic)

- Bronze – $130.15/month, $750 excess, see-u by HBF Saver Hospital $750 Excess with Daily Co-Pay (Bronze Plus)

- Silver – $167.05/month, $750 excess, Westfund Silver Plus Everyday 750 Hospital

- Gold – $248.55/month, $750 excess, Mildura Health Fund Five Star Gold $750 Excess – F4

The Lifetime Health Cover Loading adds 2% to your Hospital Cover premium for every year you’re over 30 when you first take out cover (removed after 10 years of continuous cover).

How much does Extras Cover cost?

Extras Cover helps reduce the cost of services outside hospital, like dental, physio and optical. It does not reduce your tax. For a single person in their 30s, no kids, living in Queensland as at April 2026:

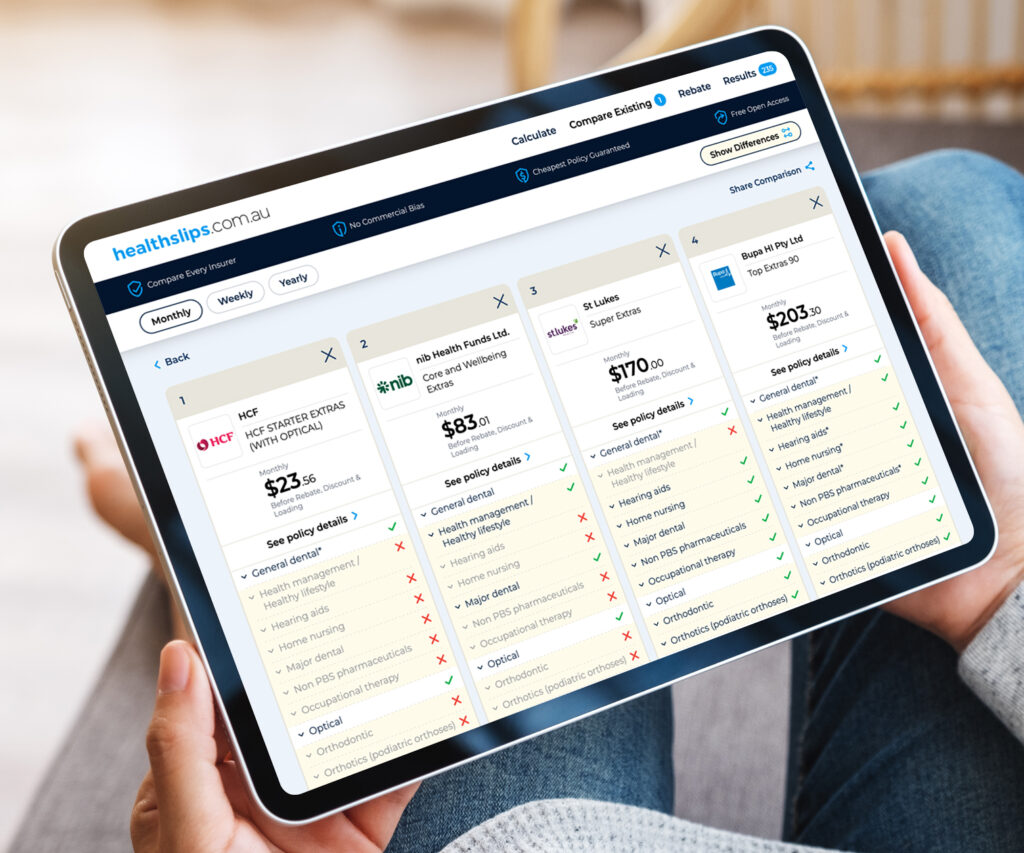

- Cheapest Extras Cover – $22.73/month, HBF Smart Start Extras, which covers 9 of 27 treatments including General Dental, Optical and Physio.

- Most Expensive Extras Cover – $200/month, Bupa Health Insurance Top Extras 90, which covers 25 of 27 treatments.

How much does Combined Cover cost?

Combined Cover includes Hospital and Extras cover. For a single adult in their 30s, no kids, living in Queensland, here are some price comparisons for Bronze Hospital tier, as at April 2026:

- Cheapest Combined Cover – $154.35/month, $750 excess, Frank Health Insurance Bronze Hospital & Bundables $250, which covers 21 of 38 Hospital Cover clinical categories and 13 of 27 Extras treatments including General Dental, Optical and Physio.

- Most Expensive Combined Cover – $364.45/month, $750 excess, Bupa Health Insurance Bronze Plus Advantage Hospital $750 Excess, which covers 28 of 38 Hospital Cover clinical categories and 25 of 27 Extras treatments.

What type of health insurance should I get?

The right cover depends on what you want it for – saving tax, reducing health costs or peace of mind.

Hospital Cover – covers treatment in a private hospital or as a private patient in a public hospital and can help you access non-urgent surgery faster. It helps you avoid the Medicare Levy Surcharge if your income is over the MLS threshold. It can also help you access private childbirth, although there’s a 12-month waiting period so you’ll need to buy your policy before getting pregnant (find out more in our Starting a Family guide).

What health treatments are covered by Hospital Cover?

Extras Cover – helps cover out-of-hospital costs not covered by Medicare such as dental, physio, optical and psychology. Extras Cover doesn’t cover all of your treatment costs and there’s an annual limit. Remember that Extras Cover does not affect the Medicare Levy Surcharge.

What health treatments are covered by Extras Cover?

Combined Cover – includes Hospital Cover and Extras Cover. It won’t save you any money, but it means you’ll only have one bill to pay for 2 types of insurance.

Ambulance Cover – Medicare doesn’t cover ambulance treatment, which is why Ambulance Cover can be useful. Ambulance treatment costs are often included with Hospital Cover and Extras Cover policies, so you probably won’t need Ambulance Only Cover if you’re buying other health insurance. (Note: if you live in Queensland or Tasmania, your state governments fund ambulance costs.)

Who should my policy cover?

- Single – one adult.

- Couple – 2 adults living together (you don’t have to be married).

- Single Parent – one adult and one or more children.

- Family – 2 adults and one or more children (you don’t have to be married).

Compare all cover types and the cost of including a partner and children in your policy using the healthslips.com.au calculator. It’s fast, easy and free.

Becky & Alex, different priorities

Becky, 31, and Alex, 33, are a couple who live together. Becky has got a promotion that will put her salary over the Medicare Levy Surcharge threshold, while Alex has been told they will need surgery for plantar fasciitis in the next few years. Alex gets a Silver tier Singles policy so they can have their surgery in a private hospital once they have served the 12-month waiting period for pre-existing conditions. Becky gets a Basic Plus Singles policy that gives her a lower level of cover but means she avoids the Medicare Levy Surcharge.

Incentives and penalties to know in your 30s

Government incentives and penalties can significantly affect how much you pay for health insurance:

- Private Health Insurance Rebate – reduces premiums if you earn below the income thresholds.

- Lifetime Health Cover Loading – adds 2% to Hospital Cover premiums for every year you’re over 30 when you first take out cover (removed after 10 years of continuous cover).

Don’t forget about the Medicare Levy Surcharge (MLS) – an extra tax (1-1.5% of income) that applies if you earn over the threshold and don’t have Hospital Cover for the full financial year.

Dev & Bella, starting later

Dev, 38, and Bella, 36, are a couple who live together. They decide to buy a Hospital Cover policy in case they need private hospital treatment in the future. Because neither has had Hospital Cover before, they each must pay Lifetime Health Cover Loading – Bella 10% and Dev 16%. They buy a Couples policy which includes a Loading of 13% – the average of Dev and Bella’s individual Loadings.

How do I choose health insurance in my 30s?

Here are 4 simple steps:

- Choose your cover type

If you want to avoid the Medicare Levy Surcharge, you’ll need Hospital Cover. If you want cover for out-of-hospital treatments like dental and physio, you’ll need Extras Cover. Choose Hospital Cover, Extras Cover or both, based on your health needs and budget.

- Choose what treatments matter

If you have a health condition, or a family predisposition to a particular illness, look for a policy that meets those needs.

- Compare policies

The healthslips.com.au calculator searches every policy in Australia without commercial bias, with free, fast access to all results.

- Buy your policy

Check waiting periods, excess and any incentives or penalties before buying. You’ll be covered once you’ve paid your first premium, but there may be waiting periods before you can claim.

Oliver, planning for prevention

Oliver is 33 and has a family history of bowel cancer. He considers a Bronze tier Hospital Cover policy that includes the Gastrointestinal Endoscopy clinical category so that he can get colonoscopies done at a private hospital, avoiding public hospital wait times. He decides to get a Combined Hospital and Extras policy so he can also claim for dental and physio treatments. He has to pay 6% Lifetime Health Cover Loading which increases his policy price, but because his income is in the lowest income bracket for the Private Health Insurance Rebate, his premiums are reduced.

Policies change monthly, stay informed

Subscribe to stay informed. Insurers regularly update policies, introduce new policies and close policies. Our data is updated monthly.